If you plan on driving your car for business, in 2023, you might be able to deduct 65.5 cents per mile. If you drive for medical reasons the rate is 22 cents per mile. For charity, it’s 14 cents per mile.

Driving the same car for business and personal use will require you to calculate the use percentage for each. The miles driven for business are deductible, but the miles driven for personal use are not.

Business Miles

There are two methods of deducting the use of your car for business. There is the standard mileage rate (65.5 cents per mile), and there is actual use.

Standard mileage covers maintenance and repairs on your car, as well as gasoline and insurance. The 65.5 cent rate is a flat rate meant to cover all these expenses. You’ll have calculate which method will give you the biggest deduction.

You can alternate between methods every year, but only if you opted to use the standard mileage rate the first year you used your car for business.

Medical Miles

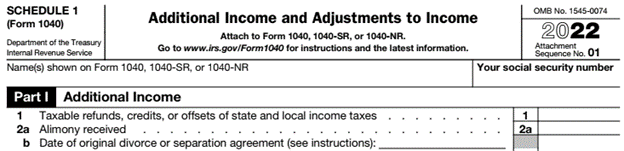

Although medical miles have a lower rate than business miles, they follow the same rules. You can either deduct the standard mileage rate (22 cents per mile) or actual expenses. Unlike business miles, which are deducted on Schedule C, medical miles can only be deducted on Schedule A, Itemized Deductions.

To figure out which medical expenses are allowed by the IRS consult Publication 502, Medical and Dental Expenses.

Charity Miles

If you used your car to provide services to a qualified charitable organization, you can either deduct mileage (14 cents per mile) or actual expenses. These expenses must be unreimbursed and out-of-pocket.

Like medical deductions, charitable deductions must also be claimed on Schedule A.

Final Note

Burden of proof lies with the taxpayer. Any car deductions claimed on the tax return must be ready to be substantiated in the case of an audit.

Miles driven, and the purpose of those miles, must be made clear to the IRS through recordkeeping.