1. A loss can only be claimed on a tax return for investment assets, not for personal assets. Personal assets are assets such as a home or car. Gains from personal assets are still taxed, but losses cannot be claimed (although an exclusion is available for the sale of a home).

2. Capital losses reduce income. Capital losses are claimed on line 7 of Form 1040 (in parentheses). They lower your income, which in turn can produce a lower tax.

3. Capital losses are limited to the lesser of $3,000 or your total net loss. To figure your capital losses you’ll first need to list your sales on Form 8949, then transfer your short-term and long-term net gains/losses to Schedule D, where you’ll figure your limit and any possible carryover losses.

If you’re one of the many people who use payment apps like Venmo and Zelle, you’ve probably heard that companies will begin reporting amounts to the IRS. There’s a lot of confusion about the new change but this article should clear most it.

Companies that use third-party payment networks have always been required to report amounts received to the IRS. The former threshold was $20,000 but the IRS brought it down to $600 in recent years. (Check out this article for more information.)

The IRS is focused on making compliant individuals and companies who fail to report income earned from business activity. Although the IRS has clarified what constitutes taxable and non-taxable, that still won’t make it easy on individuals who use payment apps for personal use and still receive Form 1099-K.

So here it goes. Amounts received through payment apps that were personal (such as gifts and reimbursements) will either have to be corrected by the company issuing the form or will have to be adjusted on your tax return.

The IRS advises taxpayers to call the issuing company (their info should be on the 1099-K) and have them correct the amount reported. If, for whatever reason, that can’t be done, you can make the correction on your tax return.

Note: Keep your original 1099-K and all copies of your communication efforts with the issuing company.

To make the correction on your tax return you’ll have to report the amount received on Schedule 1, line 8z. Then, report the same amount on the same schedule, on line 24z. This will fulfill the reporting requirement while also zeroing out the income.

Hopefully this article clarified the biggest confusion about Form 1099-K. If you have other questions the IRS has set up an FAQ page to answer questions about this form.

Taxpayers are generally allowed to exclude up to $250,000 ($500,000 if Married Filing Jointly) from gains of a home sale. There are eligibility requirements that must be met to qualify, found in IRS Publication 523. For most, those requirements boil down to whether the home was owned and used by the taxpayer for 2 out of the previous 5 years before the sale of the home. The 2 years don’t have to be continuous. You also must not have taken an exclusion for the sale of another home in the 2 years prior to selling your current home.

The exclusion alone might not be enough to exclude all gains. In order to bring those gains within the exclusion range it’s important to increase the basis of the home. Basis is your investment in the property. It includes your purchase cost and certain closing costs and improvements made before selling.

The following closing costs are allowed to be included in the basis:

Abstract fees (abstract of title fees)

Charges for installing utility services

Legal fees (including fees for the title search and preparing the sales contract and deed)

1. You’re allowed to claim the saver’s credit and take the IRA deduction on your tax return.

The Retirement Saver’s Credit is a credit available to those who’ve made contributions to their traditional or Roth IRA, as well as to employer-sponsored retirement plans. The credit is an offset on your income tax.

An IRA deduction is an adjustment to your income. It lowers your taxable income, resulting in a lesser tax.

2. You need to meet 3 requirements to claim the saver’s credit.

1. Be older than 18.

2. Can’t be claimed as a dependent by anyone.

3. Can’t be a student.

3. You can’t claim the credit if your contribution was the result of a rollover from one plan to another.

4. The credit will only apply to a maximum contribution amount of $2,000 ($4,000 for married filing jointly).

For example, if you’re single and contribute $3,500 to your retirement plan, only $2,000 will count towards the credit.

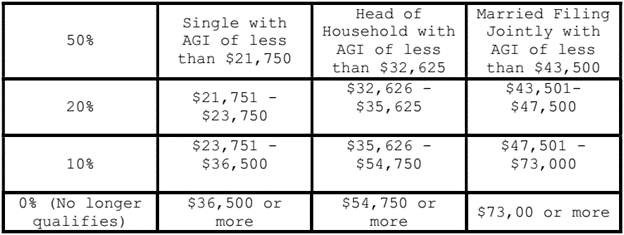

5. The amount of the credit has AGI limits.

Depending on your adjusted gross income (line 11 on Form 1040), your credit will be capped at 50%, 20%, or 10% of your contribution amount.

The following table shows the limits for 2023.

Using the previous example, if you’re single and made a $3,500 contribution only $2,000 qualifies for the credit. And if your AGI was $19,000 you’re due a credit of $1,000 (50% of contribution amount).

For more information visit the IRS’s retirement page.

There are two ways to deduct the use of a home office. You can deduct actual expenses, which provide for a higher allowable deduction. If you go this route, you’ll be bound by stricter requirements and more detailed reporting.

The IRS also allows taxpayers to use the Simplified Method. This method allows a deduction of $5 per square foot (limited to an area of 300 square feet).

The deduction is not allowed if a taxpayer has business expenses, unrelated to the use of a home office, that are greater than the gross income produced by the use of your home office.

If your business gross income is greater than your other business expenses, deduct the smaller of this difference or of the home office deduction.

Taxpayers who only had a home office for part of the year are limited to the average monthly square footage use. For example, if you started operating out of your home office in September, you’ll figure the average like this (assuming your home office use was 200 square feet):

The simplified method is particularly helpful for self-employed individuals who rent. It’s easier to figure out and requires less recordkeeping. If you’re interested in deducting actual home office expenses, you can read more about Form 8829.

It’s important, when spouses work together, that each spouse gets the social security and Medicare credit they deserve. It’s common for one spouse to file a Schedule C, claiming all income and expenses, when in fact, both spouses contributed equally to running their business.

The IRS generally requires married couples who run unincorporated businesses to file as partnerships. To limit the level of complexity, however, the IRS allows for the Qualified Joint Venture exception. This exception is available to married couples who:

1) file a joint return and are the only members of the venture.

2) materially participate in the business.

3) elect not to be treated as a partnership.

If you and your spouse qualify to file as a Qualified Joint Venture, you can each file a Schedule C. You’ll need to split the income and expenses according to each person’s interest in the business. For example, if both spouses were equally responsible and exerted the same level of control in the business it’s safe for each spouse to report 50% of the income and expenses on their respective Schedule Cs. You won’t necessarily pay more in taxes, but you will make sure each person’s social security and Medicare accounts are credited.

Note that the business must be co-owned by both spouses and must not be a state law entity. If you’ve registered the business with the state as an LLC, you no longer qualify as a Qualified Joint Venture and must file as a partnership. This involves filing Form 1065, in addition to Form 1040.

One of the biggest misconceptions of individuals who register their businesses as LLCs with the state is that they’ll now be able to “pay themselves” from their business earnings.

It’s necessary to clarify how LLCs actually work, so that individuals can make the right decisions for themselves and their businesses.

An LLC is a legal entity bound by the laws of the state it was registered in. An LLC is not by default a corporation for tax purposes. If you are the sole owner and member of your LLC you’re considered a disregarded entity by the IRS. This means that for income tax purposes you’re still considered a sole proprietor, and will still have to file a Schedule C. The only time you’re considered a corporation is when you hire employees, in which case you’ll need to apply for an EIN in order to file employer tax returns such as Form 941.

You are not obligated to remain a disregarded entity, however. The IRS offers business owners the option to become either a C corporation or an S corporation (each with their own specific tax rules and consequences).

In short, an LLC does not offer by default favorable tax treatment to sole proprietors, unless they change their classification to a C corporation or S corporation. LLCs do offer business owners some legal protection to their assets and might still be a good business option. It’s important to discuss this topic with both a lawyer and a tax professional if you’re thinking of going this route.

If you’re the personal representative of a parent who has passed away, you’ll be tasked with filing their final tax return.

The first step is to gather all their tax documents. These include documents showing income and those supporting tax deductions. It’s important to know what year your parent’s final tax return is actually due. For example, if your parent passed away November 2022, their final tax return is due April 2023. If, however, your parent passed away March 2023, and did not file for 2022, you’ll need to file tax returns for both 2022 and 2023.

If your parent’s tax return shows a tax due, you’ll be responsible for paying it. If it shows a refund, you’ll need to attach Form 1310, Statement of Person Claiming Refund Due a Deceased Taxpayer. The IRS doesn’t require a death certificate, but advices you have one for your records.

When filing the tax return, you must write at the top of the return, “DECEASED”, followed by the person’s name and date of death. If filing electronically, the software should offer a line for this information in the personal data section. The representative’s name and address go in the address section. To sign the return, write “personal representative” on the line.

The above applies to all tax returns needing to be filed by representatives. Some returns, however, are more complicated than others, and might require extensive professional help. Consult a tax professional if your parent had sources of income beyond jobs and/or pensions.

If you’re self-employed and are considering virtual currency as a payment method, you’ll be surprised to find that not much will change for you in terms of tax reporting. That being said, there’s still a few details to go over.

First, the IRS classifies virtual currency (or digital assets) as property, not cash. Virtual currency falls in line with other property like stock. So, when you provide a service and get paid with virtual currency, you’re exchanging a service for a property.

As an independent contractor, you’re still obligated to report income over $400 on your Schedule C and to pay self-employment tax on that income. The individual or company that paid you still has to report payments made to you over $600 to the IRS. In this regard nothing has changed.

The only thing that has changed is how you calculate the income you receive. In a regular cash transaction, let’s say you charge $100 for your service, the buyer pays you and you report those $100 straight on your return. If you receive virtual currency, you’ll have to report the Fair Market Value (in US dollars) of that payment. The FMV is what the currency was going for on the market on the day you received it. This makes it important to keep detailed track of your virtual receipts.

It’s possible you might not receive any tax form showing your income in virtual currency. You’ll still have to report it. For a few years now the IRS has added a question at the top of the 1040 asking if you’ve received or sold digital assets. If you got paid in virtual currency, click “Yes”. Although slowly, the IRS is cracking down on taxpayers who might owe taxes because of virtual currency transactions.

Scenario: An 18-year-old college student, who is claimed as a dependent on his parents’ tax return, decides to get a job. He wants to know how this will affect his parents’ return.

There are three main concerns when a student takes up a job while being claimed on his parents’ tax return.

#1. Can my parents still claim me?

Your parents can still claim you even if you get a job, so long as you’re still under the age of 24 at the end of the year, remain a student, and you don’t provide over half of your support. Technically, you’re supposed to live with your parents, unless the only reason you’re not is because you’re going to school.

#2. Do you have to file a tax return?

Maybe. As a dependent, there are certain filing requirements you must meet to be required to file.

If your income comes solely from a W2 job and you haven’t married, you must have made over $12,550 (for the 2022 tax year). If you made less than this, you might still want to file if a refund is in order. Which leads us to our third concern.

#3. If I file, will I owe?

How much you’ll get back or owe boils down to your standard deduction. As a dependent, your standard deduction is the larger of $1,100 or the income you earned plus $350 (but not more than $12,550).

For example, you got a summer job and made $5,600. Your standard deduction is the larger of $1,100 or $5,600 plus $350. Your standard deduction is $5,950. On a straight-forward return like this, taxable income is 0 and there’s very likely a refund.

Note: It’s important for you and your parents to be on the same page. The best course of action is to consult a tax professional before getting a job to have a higher degree of certainty of what to expect come tax time.